Australia’s per capita recession continues for fifth quarter | Australian Broker News

News

Australia’s per capita recession continues for fifth quarter

Impact of weak GDP on rates of interest

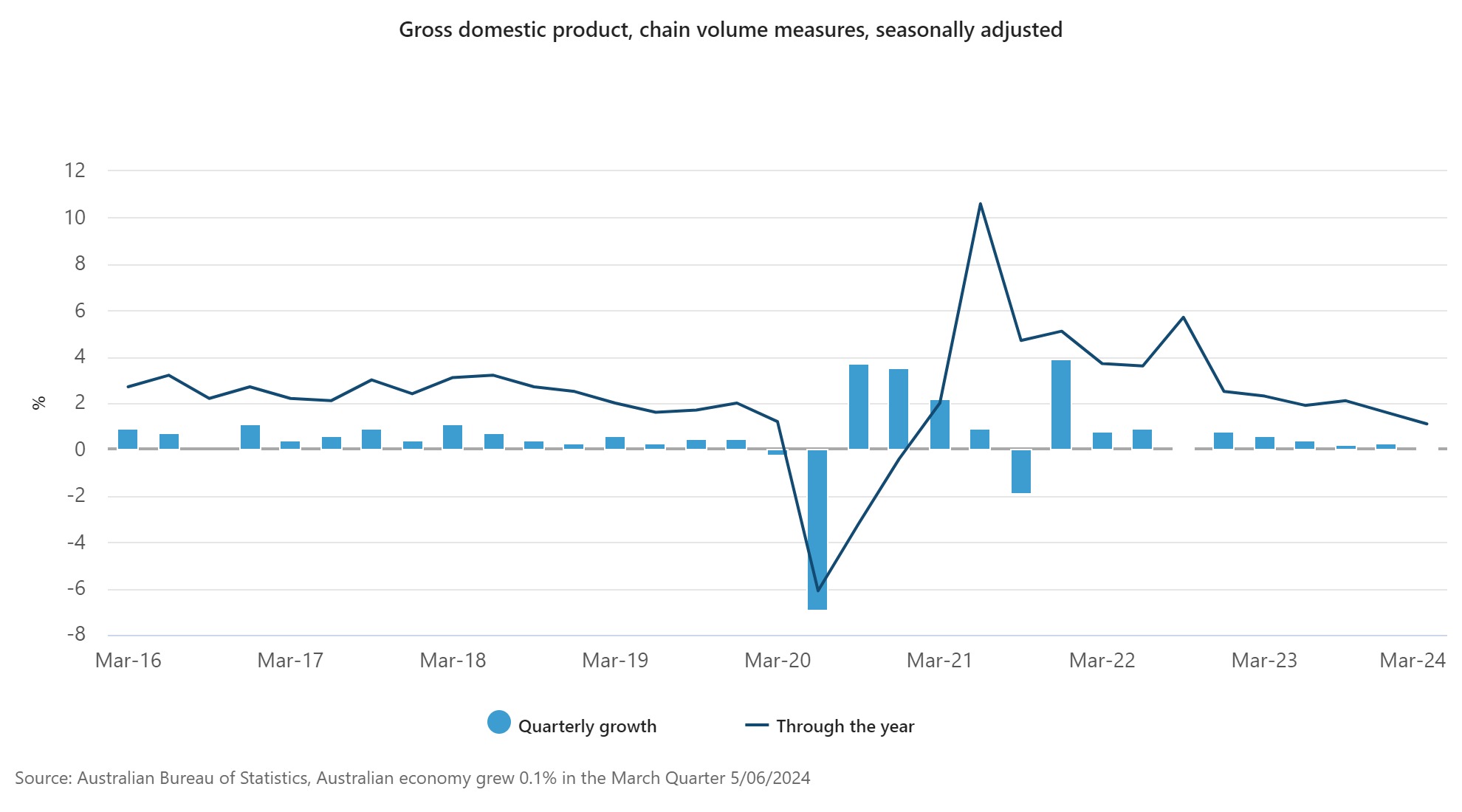

Australia’s financial development slowed considerably within the March quarter, in keeping with information launched by the Australian Bureau of Statistics (ABS).

While the general GDP managed a meagre 0.1% improve, a deeper concern lies with the continued per capita recession – a measure that reveals every individual’s share of financial output.

Katherine Keenan, ABS head of nationwide accounts, mentioned the weak March GDP figures had been the financial system’s lowest through-the-year development since December 2020 following the latest pattern.

“GDP per capita fell for the fifth consecutive quarter, falling 0.4% in March and 1.3% by means of the 12 months.”

Where GDP measures the overall market worth of all items and companies produced in a rustic, GDP per capita divides the GDP determine by the nation’s inhabitants.

Therefore, whereas Australia continues to be marginally rising its manufacturing, the slice of the pie for the typical individual has been declining for 15 months.

Impact of weak GDP on rates of interest

Weak GDP would usually immediate the Reserve Bank to decrease rates of interest to stimulate the financial system, nonetheless, sticky inflation is more likely to delay that final result.

Canstar’s finance knowledgeable Steve Mickenbecker (pictured above) mentioned debtors would welcome an early 25-basis-point rate of interest lower that might decrease month-to-month repayments on the typical $600,000 mortgage over 30 years by $101 to $3,984.

“The March quarter GDP development charge has made the already robust job for the Reserve Bank even trickier, probably setting the financial system on the trail to recession,” Mickenbecker mentioned.

“The Reserve Bank’s slender runway has turn into skinnier, with March quarter CPI development rising to 1.4% and GDP development falling to 0.1%. The Reserve Bank might be treading a fragile tightrope between avoiding recession and holding the bank card genie contained.”

The Reserve Bank is predicted to carry the money charge regular for no less than one other quarter till the subsequent spherical of quarterly inflation information is launched.

Stagflation on the playing cards?

Mickenbecker mentioned that whereas it’s too early to name, an financial system in recession and with excessive inflation awakens recollections of 1970’s stagflation.

“That put central bankers between a rock and a tough place, both tolerating larger inflation or triggering job losses. It took the world a very long time to recuperate manner again then,” he mentioned.

“Impending tax cuts and the minimal pay charge determination might throw a lifeline to the financial system and haul it again to more healthy development however will on the identical time add to inflationary pressures.”

ABS information: What else occurred?

Government spending rose

Government remaining consumption expenditure rose 1.0% in March. Both nationwide (+1.2%) and state and native (+0.8%) spending contributed to this improve.

“Government advantages for households drove the expansion in authorities spending, because the federal authorities elevated spending on medical companies and a few State governments supplied vitality invoice reduction funds,” Keenan mentioned.

Households spending on necessities rose

Household spending rose 0.4% within the March quarter.

“Essential classes like electrical energy, well being, hire and meals drove development once more this quarter.

“We additionally noticed will increase in some discretionary classes due to abroad journey and spending on playing, sporting and musical occasions,” Keenan mentioned.

Public and personal capital funding fell

Total capital funding fell 0.9%.

“Private funding fell by 0.8% pushed by a decline of 4.3% in non-dwelling funding. This was attributable to a discount in mining funding in addition to a discount within the variety of small to medium constructing tasks below development in comparison with December,” Keenan mentioned.

Total dwellings (-0.5%) and possession switch prices (-2.2%) additionally detracted from non-public capital development, reflecting falling constructing approvals and subdued exercise within the property market.

Machinery and gear partly offset these falls, rising 2.2%, after a fall final quarter attributable to elevated information centre and transport gear funding.

Public capital funding fell for the second straight quarter, pushed by decreased state and native public sector funding. Water, vitality, transport, well being and schooling infrastructure all contributed to this drop.

“Despite the falls in private and non-private funding, the extent of general funding remained excessive and continued to exceed mining funding increase ranges seen within the early 2010s,” Keenan mentioned.

Net commerce detracted from development

Net commerce detracted 0.9 proportion factors from GDP development this quarter, with stronger imports (+5.1%) than exports (+0.7%).

Goods imports rose 6.5% as consumption and capital items all elevated. Services imports rose 0.7%, pushed by transport companies, whereas journey companies noticed its second quarterly fall as travellers decreased their abroad spending.

Goods exports rose 1.1%, pushed by liquified pure gasoline, non-monetary gold and meat. These will increase had been partly offset by falls in exports of coal and different rural items. Services exports fell 1.1%, primarily attributable to a fall in journey companies.

Increased imports constructed up inventories

Change in inventories rose $2.2 billion within the March quarter, contributing 0.7 proportion factors to GDP development.

Wholesale and retail inventories run down final quarter had been rebuilt with the rise in imports. Metal ore and non-metallic mineral mining drove the rise in mining inventories, as manufacturing rose greater than demand.

This decreased demand for mining commodities led to a 5.3% fall in mining income this quarter, after a 7.9% rise final quarter.

Compensation of staff rose

Compensation of staff (COE) rose 1.0% within the March quarter, the smallest development since September 2021. This signifies slowing development within the labour market.

Private sector wages rose 0.9%, driving the expansion in whole compensation of staff, and public sector wages rose 1.6%. Pay rises and backpay throughout federal, state and territory governments contributed to this general development.

Household financial savings ratio fell

The family saving ratio fell to 0.9% within the March quarter after rising final quarter.

“Household revenue acquired grew at its lowest charge since December 2021, reflecting the comparatively small rises in compensation of staff and funding revenue acquired this quarter,” Keenan mentioned.

“Compared to final quarter, the expansion in revenue tax payable didn’t detract as a lot from whole revenue payable by households, leading to a decrease family saving ratio.”

Related Stories

Keep up with the most recent information and occasions

Join our mailing checklist, it’s free!